The use of algorithmic underwriting is increasing across the insurance industry. Algorithmic approaches to underwriting can optimize insurers’ operations and customers’ experiences by enhancing decision-making and improving risk assessment.

In this article, we dive into the evolution and benefits of algorithmic underwriting and share our insights into building and scaling algorithmic underwriting platforms.

Evolution…

Algorithms have always been part of the underwriting process, but they have generally been limited to ratings. For example, when determining risk factors for car insurance, an algorithm or mathematical formula is used to set rates based on the vehicle make, model, driver age, location and previous history. Whether simple or complex, algorithms have long been our core rating tool.

The use of algorithms in other areas of the underwriting process has been limited due to concerns that these factors overlap with rate setting, or simply that other parts of the underwriting process lack the data and analytical capabilities to make these decisions. Instead, the insurance industry often relies on complex rules engines to make decisions about risk acceptance, risk grading and reporting sequencing.

As data access and analytics tools advance, carriers are now rethinking the use of algorithms, either alone or alongside traditional rules engines, to enhance decision-making throughout the underwriting process.

How it works…

Algorithmic underwriting employs analytical models to automate decisions in the underwriting process or provide insights to assist underwriters. For more homogeneous risks, it can fully or partially automate underwriting.

Key decisions made using algorithmic underwriting:

- Determine whether the submission meets the carrier’s risk appetite

- Identify key risk characteristics, such as correct SIC/NAIC codes

- Prioritize accounts based on willingness and ability to win

- Risk determination of some or all risks

With this approach, carriers can accept or reject risks more quickly and reduce underwriting workload. It also helps provide customers with more personalized risk assessments, real-time risk management and a seamless experience.

5 Advantages of Algorithmic Underwriting

Algorithmic underwriting greatly benefits the insurance industry in 5 key areas:

- Process efficiency: By automating the underwriting process, we have found that algorithmic underwriting reduces processing time by up to 50%, streamlines operations, increases testing speed, and simplifies maintenance of complex decision-making systems. In addition, automated processes for algorithmic underwriting can help cope with up to 25% increases in the number of applications reviewed, allowing insurers to increase premiums without increasing operating costs.

- accuracy: The accuracy of risk assessments can be improved by analyzing wider data sets. These analyzes help identify patterns and correlations that might be missed by human underwriters alone. By enhancing underwriters’ insight and judgment, errors in risk assessment can be minimized and fraud can be more easily detected. We estimate that fraud losses could be reduced by up to 30% for some insurance companies.

- price: By enhancing risk assessment, pricing decisions can be more accurate. Algorithmic underwriting helps tailor premiums to individual risk profiles, improving customer satisfaction and competitiveness. In addition, it supports dynamic pricing, adjusting premiums in real time based on changing risk factors, which we believe can increase underwriting profitability by up to 20%.

- Proactive risk management: Algorithms can help insurers proactively identify emerging risks and adjust their underwriting and risk management strategies. This helps mitigate potential losses, lower loss ratios and improve overall portfolio performance.

- Customer experience: Algorithmic underwriting can make instant or near-instant decisions about coverage eligibility, pricing, and personalized offers. Through predictive and prescriptive analytics, insurance companies can provide real-time, contextualized quotes that make insurance more accessible and more relevant to individual customers’ needs. It also makes insurance more accessible to customers or segments that may have been marginalized by past underwriting methods.

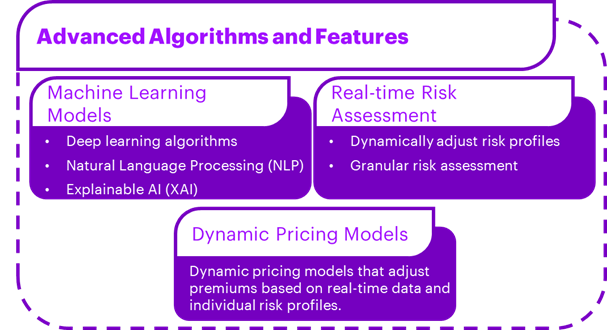

Building an algorithmic underwriting platform at scale

Algorithmic underwriting platforms need to adopt a multi-layered approach and consider future scalability. Advanced capabilities required when considering an algorithmic underwriting platform include machine learning models, real-time risk assessment, and dynamic pricing models.

Challenges to consider when optimizing your data and algorithm underwriting platform:

- Data quality and availability: Data may be fragmented, incomplete or out of date.

- Model interoperability: Complex machine learning algorithms used for underwriting can lack transparency and interoperability, making results difficult to interpret.

- obey: As regulation of algorithmic models and AI increases, insurers must stay ahead of the curve and adapt their models as needed.

- Fairness and Prejudice: If not proactively addressed, algorithmic underwriting may create the risk of unfair practices and historical biases being perpetuated.

- Data Privacy and Security: Algorithmic underwriting involves the collection, processing and storage of large amounts of personal and sensitive data. Protecting customer data is critical to compliance and maintaining customer trust.

Success stories…

We are seeing successful examples of algorithmic underwriting across the industry. Take property insurance as an example, gas insurance Leverage artificial intelligence and algorithms for instant business insurance quoting and automated policy issuance. hiscox Worked with Google Cloud to develop artificial intelligence models that automate underwriting of specific products. Meanwhile, in terms of life insurance, Spirit Leverage machine learning to assess risk and provide streamlined insurance applications.

in conclusion

While algorithmic underwriting is not a new concept in the insurance world, it is revolutionary in terms of enhanced access to new data sources, improved data quality, and better analytical tools. These enhancements enable underwriters to gain insight into other areas of the value chain and extend their capabilities beyond archaic models or obsolete rules.

Despite their complexity, insurers need to be aware of potential bias and lack of transparency in algorithmic underwriting models. Ethics and compliance, including data privacy, consumer protection and fair lending laws, will present challenges for insurers from the outset.

As technology continues to evolve and data analytics capabilities expand, we are witnessing how algorithmic underwriting will revolutionize the insurance industry, driving innovation and helping financial institutions make smarter, data-driven decisions.