Generative artificial intelligence (GenAI) has the potential to transform the insurance industry by providing underwriters with valuable insights into: 1) Risk control, 2) building and location details and 3) underwriting operations. The technology can help underwriters identify more value during the submission process and make better quality, more profitable underwriting decisions. The improved rating accuracy of CAT modeling means better, more accurate pricing and reduced premium leakage. In this article, we will explore the areas of opportunity for GenAI, GenAI capabilities, and the potential impact of using GenAI in the insurance industry.

1) Risk control insights Material data area

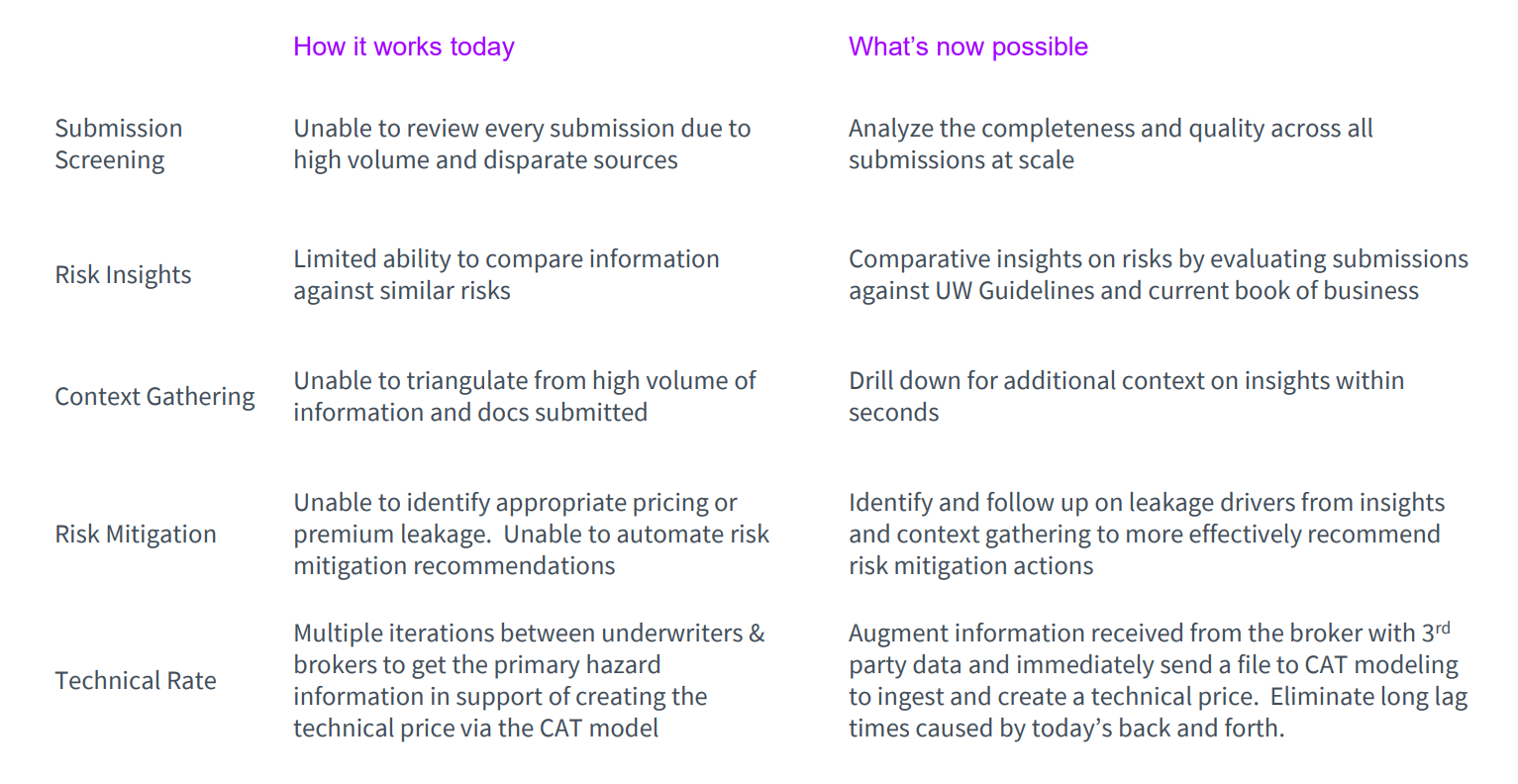

Generative AI allows rRisk control analysis insights are highlighted to show existing loss prevention measures and the effectiveness of these controls in reducing potential losses. These are critical to informed underwriting decisions and can address areas or pain points that underwriters have been missing in the data collection process. Currently, with regard to submission screening, underwriters are unable to review every submission due to the large volume and disparate sources of submissions. Generative AI enables them to Analyze the completeness and quality of all submissions at scale. This means they move from a limited ability to compare information with similar risks to a situation where they have comparative insights into risks by evaluating submissions against UW guidelines and current business manuals.

What generative AI can do:

- Generate a comprehensive narrative of overall risk and its alignment with carrier preferences and books

- Mark, source and identify required missing material data

- Manage the lineage of updated data

- Enriched from secondary sources TPA/external data (e.g. publicly listed products/services operated by the insured)change)

- Validate submitted data against these additional sources (e.g., geospatial data to verify vegetation management/proximity of building and roof construction materials)

Synthesizing submission packages with third-party data in this way can be presented in a meaningful, easy-to-consume way that ultimately aids decision-making. All of these are okAbility to provide faster, improved pricing and risk mitigation recommendations. Augmenting the information received from brokers with third-party data can also eliminate the long lag times caused by today’s back-and-forth between underwriters and brokers. This can happen instantly for every commit simultaneously and prioritize the entire project portfolio in seconds. What an underwriter might do in a week can be done immediately and consistently while making smart, structured recommendations. underwriter Control gaps will be immediately understood based on the details submitted, and where there may be significant deficiencies/gaps that could impact potential losses and technical pricing. Of course, tThese factors must then be considered in conjunction with each insured’s individual risk appetite. These improvements ultimately create the ability to cover more risk without paying exorbitant premiums; saying “yes” when you might say “no.”

2) Building and location details insights help improve risk exposure accuracy

Let’s start with To illustrate building detailed insights, our insurance company is underwriting a restaurant chain with multiple properties.. this Chain restaurants are located in CAT-prone areas such as Tampa, Florida. How can these insights be used to supplement submissions to ensure underwriters have a complete picture of the situation to accurately predict risk exposure associated with that location? According to FEMA’s National Risk Index, Tampa’s high-risk disasters are hurricanes, lightning and tornadoes. in this casethis Insurance companies have A medium risk level has been imposed on restaurants due to the following reasons:

- Past security checks failed

- Lack of hurricane protection

- Potential links between past maintenance failures and loss events

This all adds to the risk.

On the other hand, in order to deal with these dangers, restaurants have implemented several mitigation measures:

- Mandatory hurricane training for every employee

- Each window has metal storm shutters

- Secure outdoor items such as furniture, signage, and other loose items that may become projectiles in strong winds

These have been added to the submission to demonstrate that they have taken the necessary response measures to reduce the risk.

Construction detail insights reveal what is truly insured, while location detail insights show the context within which a building operates. rightISK Control Analysis in Building Assessment and Safety Inspection Report Reveals Insights show which locations are experiencing the greatest losses, whether past losses were due to underwriting risks or control deficiencies, and the adequacy of existing control systems. Take chain restaurants as an example, It does not have its own hurricane protection, but according to detailed geolocation data, the building is approximately 3 miles from the nearest fire station. What this really means is that in terms of context gathering, underwriters go from being unable to triangulate from the reams of information and documents submitted to being able to drill down into more context on the insights in seconds. This in turn enables underwriters to identify and track leakage drivers based on insights and contextual gathering to more effectively recommend risk mitigation measures.

3) Operational insights Help provide recommendations for additional risk controls

The insured business details are a combination of information submitted by the broker, financial statements, and information not included in the broker’s Accord form/application. timehe Hazard level Information will also be provided for each location associated with the insured’s operations, as well as primary and secondary SIC codes. From this point of view, You will be able to instantly view your loss history and where you drove with the highest losses compared to your total risk.

If we take our restaurant chain example again, it will likely be attributed a “high” risk value instead of the “medium” risk value mentioned earlier due to the fact that think There are potential risks such as catering delivery operations at this location. By analyzing operational risks, we can identify high risks in the catering industry:

It has a maximum capacity of 1,000 people and is located within a shopping mall. The number of claims and average claim amounts over the past 10 years may also indicate a higher risk of accidents, property damage, and liability issues. Although some risk controls may have been implemented, e.g. OSHA compliance training, security, hurricane and fire drill response training every 6 months, mayfFurther controls are required, such as specific risk controls for catering operations and fire safety measures for outdoor open-fire pizza ovens.

This supplementary information is invaluable in calculating actual risk exposure and in attributing the correct level of risk to a client’s situation.

The benefits of generative AI extend beyond more profitable underwriting decisions

These insights not only help make more profitable underwriting decisions, they also provide additional value as they Teach new underwriters (in significantly reduced time) data/guidance and risk insights. They improve analysis/rating accuracy and reduce actuarial/pricing/ Risk Information Underwriting.

Please see the one below Let’s review Gen AI’s potential impact on underwriting:

in our latest Artificial intelligence for everyone From perspective, we discuss how generative AI will transform work and reshape business. These are just 3 ways Insurance underwriters can gain insights from generative AI. Watch this space to see how generative AI will transform the entire insurance industry over the next decade.

If you would like to discuss this in more detail please contact me here.